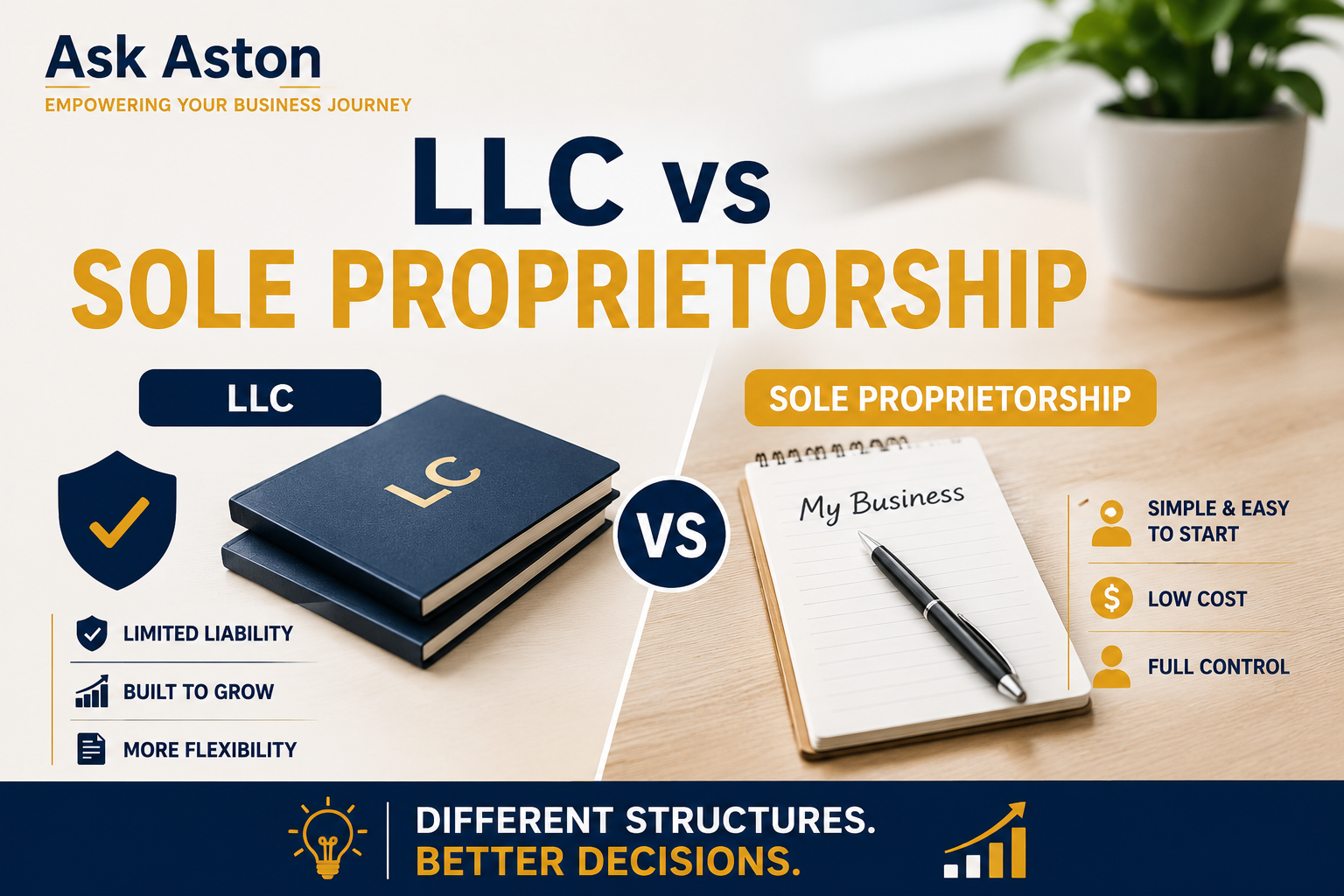

Choosing a business structure is one of the first major decisions entrepreneurs make when starting a business. Two of the most common options are a Sole Proprietorship and a Limited Liability Company (LLC). Both structures allow you to operate a business, but they differ in important ways, including liability protection, taxes, paperwork, and long-term flexibility.

Understanding the differences can help you choose the structure that best fits your goals and level of risk.

What Is a Sole Proprietorship?

A sole proprietorship is the simplest business structure available. In fact, if you start a business and do not formally register another business entity, you are typically considered a sole proprietor by default.

Under a sole proprietorship, the business and the owner are legally the same entity. The owner receives all profits, makes all decisions, and is personally responsible for all business debts and obligations.

Many freelancers, consultants, and small service-based businesses begin as sole proprietorships because they are easy and inexpensive to start.

Advantages of a Sole Proprietorship

One of the biggest benefits of a sole proprietorship is simplicity.

There is usually little paperwork required to begin operating, and startup costs are often minimal. Business income is reported directly on the owner’s personal tax return, making tax filing relatively straightforward.

Sole proprietors also maintain complete control over business decisions without needing to consult partners, shareholders, or board members.

For entrepreneurs testing a small business idea or side hustle, this simplicity can be very appealing.

Disadvantages of a Sole Proprietorship

The primary drawback of a sole proprietorship is personal liability.

Because the business and owner are legally the same, personal assets such as savings accounts, vehicles, and even a home may be at risk if the business faces lawsuits or significant debts.

This risk becomes more important as a business grows, hires employees, works with customers, or takes on financial obligations.

Sole proprietorships may also appear less established to lenders, investors, and some customers compared to formally registered business entities.

What Is an LLC?

A Limited Liability Company, or LLC, is a legal business entity created by filing formation documents with the state.

An LLC separates the business from the owner in many legal situations. While owners still manage and profit from the business, the LLC itself becomes a distinct legal entity.

This structure is extremely popular among small business owners because it combines liability protection with relatively simple management requirements.

Advantages of an LLC

The biggest advantage of an LLC is liability protection.

In many situations, the owner’s personal assets are protected from business debts and legal claims. While there are exceptions, this protection can provide significant peace of mind for entrepreneurs.

An LLC can also enhance credibility. Customers, vendors, and financial institutions often view registered business entities as more professional and established.

Additionally, LLCs offer flexibility in taxation and ownership structure, making them attractive for businesses with long-term growth plans.

Disadvantages of an LLC

While LLCs offer valuable benefits, they also involve additional responsibilities.

Most states require filing fees to create an LLC, and some charge annual renewal fees or reporting requirements. There may also be additional paperwork compared to a sole proprietorship.

Although these costs are often reasonable, they should be considered when evaluating whether forming an LLC makes sense for your business.

For very small businesses with limited risk exposure, the extra administrative work may not feel necessary at first.

Comparing Liability Protection

The most significant difference between these two structures is liability protection.

A sole proprietor is personally responsible for business obligations, while an LLC generally creates a legal separation between personal and business assets.

For businesses that interact with customers, provide professional services, sell products, or face potential legal risks, this protection is often a major reason entrepreneurs choose an LLC.

The greater the potential risk, the more valuable liability protection becomes.

Which Structure Is Right for You?

The best choice depends on your business goals, industry, and risk level.

A sole proprietorship may work well if you are starting a small side business, testing a concept, or operating with very little financial risk. The simplicity and low cost can make it an attractive starting point.

An LLC may be a better option if you want liability protection, plan to grow your business, seek financing, or want a more professional business structure from the beginning.

Many entrepreneurs start small and eventually transition from a sole proprietorship to an LLC as their business expands.

Choose the Structure That Supports Your Goals

There is no single business structure that works for everyone. Both sole proprietorships and LLCs offer advantages depending on your situation.

The key is understanding the tradeoffs between simplicity and liability protection. By choosing the structure that aligns with your business goals and risk tolerance, you can create a stronger foundation for future growth. Click the link if you want more information on business structures for entrepreneurs. The IRS also has information about business structures such as LLCs and Sole Proprietorships that might prove useful.

Need help deciding which business structure is right for your startup?

Try Ask Aston to brainstorm ideas, validate opportunities, create business plans, and get step-by-step guidance tailored to your goals.